Obama mentions oil, Keystone in State of the Union

President Obama touched on several aspects of the energy debate during Tuesday night’s State of the Union Address, including:

Imported oil:

More of our kids are graduating than ever before; more of our people are insured than ever before; we are as free from the grip of foreign oil as we’ve been in almost 30 years.

Ramped-up U.S. oil production:

At this moment — with a growing economy, shrinking deficits, bustling industry, and booming energy production — we have risen from recession freer to write our own future than any other nation on Earth.

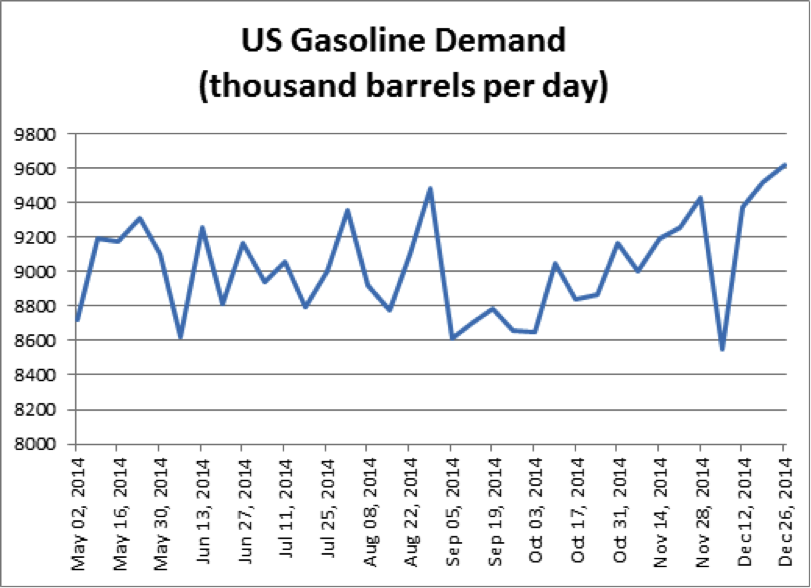

Consumers savings from cheap gasoline:

We believed we could reduce our dependence on foreign oil and protect our planet. And today, America is number one in oil and gas. America is number one in wind power. Every three weeks, we bring online as much solar power as we did in all of 2008. And thanks to lower gas prices and higher fuel standards, the typical family this year should save $750 at the pump.

The debate over the TransCanada Keystone XL pipeline:

21st century businesses need 21st century infrastructure — modern ports, stronger bridges, faster trains and the fastest internet. Democrats and Republicans used to agree on this. So let’s set our sights higher than a single oil pipeline. Let’s pass a bipartisan infrastructure plan that could create more than thirty times as many jobs per year, and make this country stronger for decades to come.

And something else about solar power:

I want Americans to win the race for the kinds of discoveries that unleash new jobs — converting sunlight into liquid fuel …

As The New Republic noted, it was the first time in his six SOTU Addresses that Obama mentioned Keystone:

It’s not surprising he’d weigh in now, given how Keystone has dominated the first few weeks of debate in the new Republican Congress. Lately, Obama has sounded skeptical of the pipeline’s economic benefits, but we still don’t have many clues as to how he will decide Keystone’s final fate in coming months.

(Photo: WhiteHouse.gov)